Wall Street Journal has a good story today on Hong Kong's real estate boom fueled partly by the Fed's easy monetary policy. This is a classic example where monetary policy of a fixed-exchange-rate regime lost its independence and the impact of US monetary policy thus spread worldwide,

Adding to the problem is rapidly appreciating Chinese Yuan against US dollar, thus Hong Kong dollar, offers extra incentives for mainland investor to move their money into Hong Kong.

HONG KONG -- For months, Fion Lau and her boyfriend have been eyeing a small apartment here. But, with Hong Kong property prices climbing at double-digit percentage rates since this past summer, she has held off buying, waiting for the market to cool.

It hasn't, but the 25-year-old marketing assistant recently bought the place anyway. That's because two weeks ago and half a world away, the U.S. Federal Reserve cut interest rates again, hoping to stimulate an economy dragged down by a housing sector in disarray. Since Hong Kong pegs its dollar to the U.S. currency, it followed the Fed's lead, knocking the city's base rate down twice in less than two weeks for a total of 1.25 percentage points.

![[Hong Kongs central district]](http://s.wsj.net/public/resources/images/AI-AN182_HKPROP_20080212135602.jpg) |

| A picture taken from the roof of Two International Finance Centre, Hong Kong's tallest building, shows the city's Central district. |

The unintended result: home-loan rates so cheap that they are throwing more fuel on an already scalding property market.

A typical mortgage here -- which is pegged to the prime rate which, in turn, is tied to the base rate -- now carries interest of about 3.1%. But compared with Hong Kong's inflation rate of about 3.8%, which is hovering at a more-than-nine-year high, that looks especially inviting, creating a so-called negative real interest rate.

For many potential home buyers in Hong Kong, mortgage payments are now effectively cheaper than rents, which are slower to adjust to rate changes. Indeed, within hours of the Fed's latest rate cut, Ms. Lau was on the phone with the owner of the apartment in the Kowloon district of Hong Kong and signed the contract to buy it that night. She says she plans to rent the flat out to tenants for two years to make money on the mortgage/rent spread and then may move in herself.

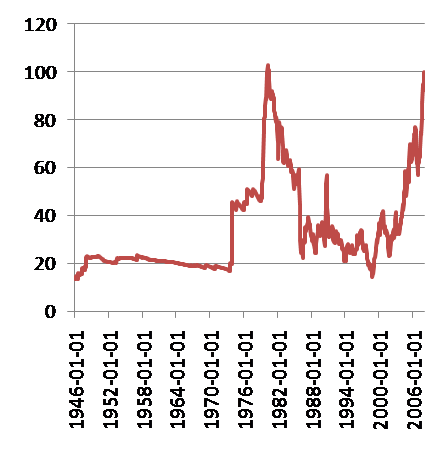

Real interest rates have been in negative territory before here in China's international-finance hub. During the early 1990s, cheap home loans helped inflate a property bubble that hit records before bursting, with devastating effect, during the Asian financial crisis of 1997-1998. Prices have only now begun to touch those levels again, and further gains could be in the cards.

Andrew Fung, head of investment and insurance for Hang Seng Bank in Hong Kong, calls the property market here one of two "certain investments" -- along with the appreciation of China's currency, the yuan -- in an uncertain economic environment. Underlying the property-buying enthusiasm: fast-rising wage increases, unemployment near its record low and bank deposits growing at about 20% a year.

Then there's the weakness of Hong Kong's dollar, which is tracking the U.S. dollar's decline. Mr. Fung credits the cheap currency with making properties even more attractive to foreign private-equity funds.

![[Hong Kong property charts]](http://s.wsj.net/public/resources/images/AI-AN177_HKPROP_20080212130012.gif)

"A couple of years ago, lots of funds were pouring their money into Singapore's residential market, and now we're seeing them buying in Hong Kong," says Keith Yeung, a senior director and head of greater China property for Merrill Lynch in Hong Kong. Also pushing up the market, Mr. Yeung says, are speculators from mainland China looking for new places to put their money.

Finally, new supply is tighter than ever before. According to property broker CB Richard Ellis, home prices in 2008 will rise another 20% or so in both the luxury and mass markets. The number of new units in the luxury residential market fell to 70 in 2007 from 1,055 units in 2005. In the mass residential market, new supply fell 44% in 2007 from the year before to more than 8,700 units.

That tight supply has helped push prices for luxury properties up 38% in the past year alone, with fresh reports of eye-popping transactions grabbing headlines every few months last year. In November, one 7,000-square-foot penthouse apartment fetched $36 million, or about $5,140 a square foot. A few months earlier, a luxury house on Hong Kong's Victoria Peak sold for $27 million, or about $5,270 a square foot. Prices in the mass market, which is comprised of the nonluxury properties, grew quickly as well in 2007, though at a more modest rate of 14% -- a sign, analysts say, that even more growth lies ahead.

Now, with inflation eating away at bank-deposit returns and volatility hitting the stock market, interest rates are giving Hong Kong residents another incentive for putting their cash into real estate, a classic hedge against inflation.

"With so many favorable factors in place, the housing sector is likely to heat up further," says Gordon Tse, corporate-development director at Midland Realty in Hong Kong, a big local brokerage firm. But, he adds, "exactly how hot it will get is difficult to predict."

Does that mean a bubble is in the offing?

![[Hong Kong home prices chart]](http://s.wsj.net/public/resources/images/AI-AN180_HKPROP_20080212135614.gif)

Analysts are urging home buyers to be cautious since interest rates could continue to fall. A bubble is "absolutely possible," says Nicholas Kwan, regional head of research for Standard Chartered Bank here. If rates drop even more sharply in 2008, which Mr. Kwan says is possible, the market could at some point begin to overheat. "But it's so hard to say where that point is," he says.

The average price of mass-residential apartments in Hong Kong rose 10.3% to roughly $593 a square foot in December from about $537 a square foot in June, according to CBRE Research in Hong Kong.

Much also will depend on where inflation and interest rates are in relation to each other. While most analysts see inflation staying high in China for some time, pushed up by more expensive commodities, interest-rate movements are going to be decided, for the most part, in the U.S. That, in turn, will depend on the condition of the U.S. economy, a broader and more important variable than interest rates alone.

"Negative real interest rates is a plus, but it's not everything," says Steve Chow, a corporate credit analyst at ING Wholesale Banking who covers the property sector. The "economic outlook is equally important for potential buyers, since buying an apartment is a major decision in many people's lives." And lately, the global economic outlook is looking wobbly, he adds.

Some Hong Kong market watchers point out that interest-rate cuts had long been expected here and that the lessons of the 1990s bubble are still seared in the city's collective memory, serving to temper further excesses.

Also, property owners are generally far less leveraged than they were a decade ago, with mortgage payments currently accounting for an average of 35% of disposable income, compared with an average of 92% in the 1990s, according to Oscar Leung, a senior investment manager at ING Investment Management in Hong Kong. Back then, cheap home loans were also accompanied by ample new supply in the market, a far cry from today's slow trickle of newly constructed apartments.

"This is a healthier market," Mr. Leung says.

--

**************************************

Paul D. Deng

Department of Economics

Brandeis University

IBS, MS 032

Waltham, MA 02454

http://www.pauldeng.com

![[Chart]](http://s.wsj.net/public/resources/images/MI-AP160_AOT_20080219193227.gif)

![[Chart]](http://s.wsj.net/public/resources/images/MI-AP175_AOT_20080220184013.gif)

![[Hedged Bet]](http://s.wsj.net/public/resources/images/MI-AP135_HOWARD_20080218193623.gif)

![[George Soros]](http://s.wsj.net/public/resources/images/HC-BZ289A_Soros_20051011151715.gif)

![[Chart]](http://s.wsj.net/public/resources/images/MI-AP157_AOT_20080218192024.gif)

![[Robert Shiller]](http://s.wsj.net/public/resources/images/HC-DW830_Shille_20051025002842.gif)

![[Charles Calomiris]](http://s.wsj.net/public/resources/images/HC-FM401_Calomi_20051017141644.gif)

![[chart]](http://s.wsj.net/public/resources/images/NA-AP420_Capita_20080213200415.gif)

![[Real Estate Stocks]](http://s.wsj.net/public/resources/images/MI-AP096_WSTOX_20080213193634.gif)

![[chart]](http://s.wsj.net/public/resources/images/NA-AP410_ECONOM_20080212183651.gif)

![[Safety Net]](http://s.wsj.net/public/resources/images/NA-AP328_JEXPOR_20080204193215.gif)